Brought to you by Kapnick Insurance Group

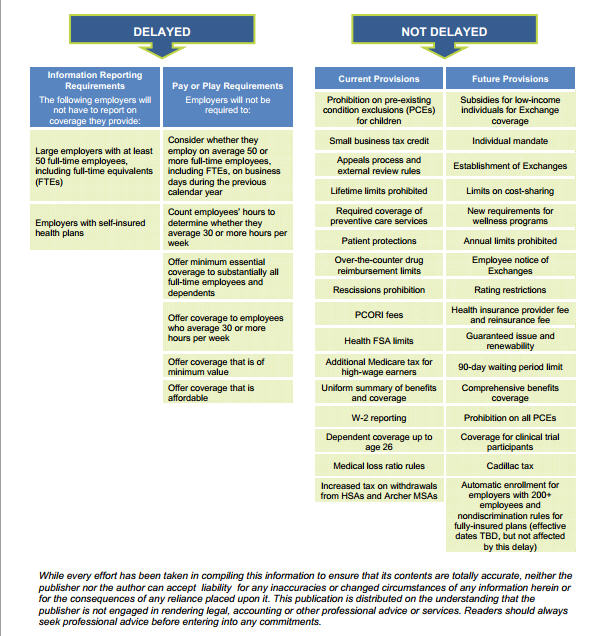

On July 9, 2013, the Internal Revenue Service (IRS) issued Notice 2013-45 to provide formal guidance on the delay of the Affordable Care Act (ACA) large employer “pay or play” rules and related information reporting requirements. The provisions affected by the delay are:

- § 4980H employer shared responsibility provisions;

- § 6055 information reporting requirements for insurers, self-insuring employers and certain other providers of minimum essential coverage; and

- § 6056 information reporting requirements for applicable large employers.

For 2014, compliance with the information reporting rules is completely optional and the IRS will not assess penalties under the pay or play rules. Both the information reporting and the employer pay or play requirements will be fully effective for 2015.

Information Reporting Requirements

The ACA amended the Internal Revenue Code (Code) to require large employers, health insurance issuers and selffunded plan sponsors to report information about health plan coverage to the IRS so that the federal government can enforce the employer mandate.

Code § 6055 requires annual information reporting by health insurance issuers, self-insuring employers, government agencies and other providers of health coverage. Code § 6056 requires annual information reporting by applicable large employers related to the health coverage that the employer offers (or does not offer) to its full-time employees.

Employer Shared Responsibility Requirements

Under the ACA, large employers that do not offer their full-time employees (and dependents) health coverage that is affordable and provides minimum value may be subject to penalties. The ACA’s employer mandate provisions are also referred to as the employer shared responsibility or pay or play rules.

One-Year Implementation Delay

The large employer pay or play rules and related reporting requirements were set to take effect in 2014. However, on July 2, 2013, the Treasury announced that these will be delayed for one year, until 2015. This means that:

- Information reporting under §§ 6055 and 6056 will be optional for 2014 and no penalties will be applied for failure to comply with these requirements for 2014; and

- No employer shared responsibility payments will be assessed for 2014.

However, both the information reporting and the employer pay or play requirements will be fully effective for 2015.

The IRS issued Notice 2013-45 to provide more information on the delay.

According to the IRS, the delay of the reporting requirements provides additional time for input from employers and other reporting entities in an effort to simplify these requirements, consistent with effective implementation of the ACA. This delay is also intended to provide employers, insurers and other providers of minimum essential coverage time to adapt their health coverage and reporting systems.

The delay of the employer mandate penalties was required because of issues related to the reporting requirements. Because the reporting rules were delayed, the Treasury believed it would be nearly impossible to determine which employers owed penalties under the shared responsibility provisions.

The pay or play regulations issued earlier this year left many unanswered questions for employers. The IRS highlighted several areas where it would be issuing more guidance. Presumably, the additional time will give the IRS and Treasury the opportunity to provide more comprehensive guidance on implementing these requirements.

Effect on Other ACA Provisions

The delay does not affect any other provision of the ACA, including individuals’ access to premium tax credits for coverage through an Exchange and the individual mandate.

Individuals will continue to be eligible for the premium tax credit to purchase coverage through an Exchange as long as they meet the eligibility requirements (for example, their household income is within a specified range and they are not eligible for other minimum essential coverage).

Future Guidance

Proposed rules for the information reporting provisions are expected to be published this summer. The proposed rules will reflect the fact that transition relief will be provided for the information reporting requirements.

It is still unclear how the new deadline will impact guidance that has already been issued, such as the transition relief for non-calendar year plans and the optional safe harbor for determining full-time status. Future guidance may affect these and other rules under the ACA.

What This Means for Employers

The Obama Administration’s decision to delay the employer mandate penalties and related reporting requirements will have a significant effect on many employers. See below for an overview of the ACA provisions that are affected by the delay, the provisions that are not affected by the delay and steps that employers are encouraged to take in 2014.